For most businesses today, accepting credit cards is no longer optional—it’s essential. In fact, according to the Federal Reserve, more than 60% of consumer payments in the United States are now made with cards, and that number continues to grow each year.

For medical offices, dental clinics, veterinary practices, and other professional practices, electronic payments have become especially important as patients increasingly expect convenient ways to pay balances, deposits, and treatment plans.

But while digital payments bring convenience and faster collections, they also come with a complex web of processing fees. Many practices assume these costs are fixed and controlled entirely by the card networks. In reality, that is not always the case.

Some payment processors quietly inflate their profits through tactics that most practices never notice—one of the most common being a practice often referred to as “enhanced billing.”

Understanding how these practices work can help protect your organization from paying more than necessary.

Understanding Interchange Fees

To understand where hidden costs can appear, it helps to first understand interchange.

Interchange is the fee that card networks such as Visa and Mastercard require to be paid to the card-issuing bank every time a credit card transaction occurs. These fees are standardized and published by the card brands.

Interchange rates vary depending on factors such as:

Card type (debit, credit, rewards, commercial)

Method of payment (swiped, inserted, tapped, online)

Industry category

Data submitted with the transaction

There are hundreds of different interchange categories, each with a specific rate and qualification requirement.

For example, a standard consumer card transaction might qualify for an interchange rate around 1.50%–2.00%, while certain reward cards or downgraded transactions may exceed 2.60% or more.

According to industry estimates, U.S. businesses pay more than $160 billion annually in card processing fees, making it one of the largest operational expenses for many organizations.

Because the system is so complex, many practices rely on their payment processor to explain how these fees work.

Unfortunately, that trust is sometimes misplaced.

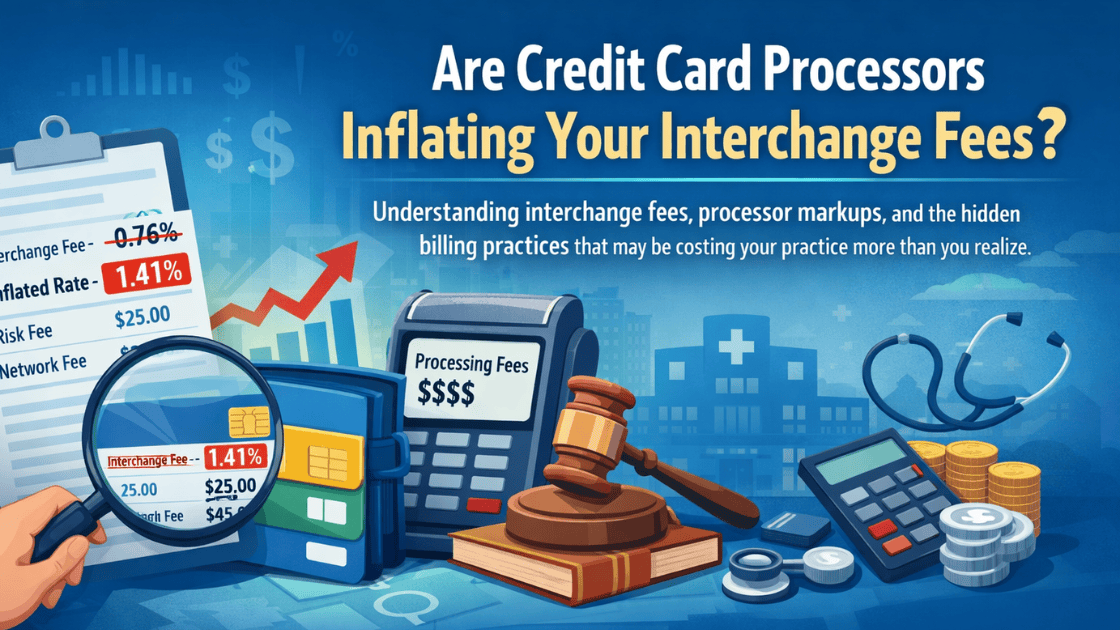

The Problem: “Enhanced Billing”

Some processors use a strategy often referred to as enhanced billing.

In this model, the processor initially advertises a very low discount rate to win the practice’s business. However, once transactions begin processing, the processor quietly inflates certain interchange categories or adds hidden markups.

Most practices never notice because they are unfamiliar with the hundreds of interchange categories and their actual rates.

For example:

The legitimate Visa interchange rate might be 0.76%

The processor adds an additional 0.65% markup

The practice sees a combined rate of 1.41% and assumes that is Visa’s fee

Without deep knowledge of interchange tables, it is difficult to know whether the rate being charged is accurate.

The Downgrade Trap

Another way processors increase revenue is through interchange downgrades.

A downgrade occurs when a transaction fails to qualify for its lowest interchange category. When that happens, the transaction moves to a more expensive category.

Common reasons for downgrades include:

Missing transaction data

Incorrect payment gateway configuration

Delayed settlement

Improper equipment setup

Manually keyed transactions when card-present options were available

For example:

| Transaction Scenario | Interchange Rate |

|---|---|

| Properly qualified card transaction | ~1.90% |

| Downgraded transaction | ~2.95% |

If a processor sets up a practice’s equipment incorrectly or fails to optimize their system, transactions may downgrade more frequently.

The result?

Higher costs for the practice—and higher profits for the processor.

In other words, the processor may financially benefit when the practice’s transactions process inefficiently.

Why Most Practices Never Notice

There are several reasons these issues often go undetected.

Statements Are Extremely Complex

Processing statements often contain dozens or even hundreds of line items, many with technical names that are difficult to interpret.

Interchange Tables Are Difficult to Navigate

Visa and Mastercard publish interchange tables, but they are long technical documents that most practices never review.

Small Changes Are Hard to Detect

Processors sometimes raise fees by only a few basis points at a time. These changes may appear small but can generate significant additional profit across thousands of accounts.

Network Changes Can Also Be Used as Cover

Visa and Mastercard typically update interchange rates twice per year, usually in April and October.

These changes are often minimal—sometimes less than one-hundredth of a percent.

However, processors sometimes use these announcements as justification to raise their own fees, attributing the increases to the card networks even when the change came from the processor itself.

Practices often notice these adjustments appearing on statements in May and November.

When you see fee increases during these periods, it is important to request a detailed breakdown of exactly what changed and why.

Fee Names Can Be Misleading

Another tactic involves creating fees that sound legitimate but are actually processor-created charges.

For example, statements might include items such as:

Risk Fees

Network Fees

Regulatory Fees

Assessment Adjustments

Some of these names resemble legitimate network charges.

However, the real card-brand fees may be only fractions of a cent per transaction, while a processor may apply a much larger fee using a similar name.

To verify legitimacy, practices should always check whether a fee appears on the official Visa or Mastercard fee schedules, not just on a processor’s website.

Legal Scrutiny in the Industry

These practices have drawn increased scrutiny in recent years.

In 2016, a class-action lawsuit was filed against Vantiv Integrated Payments alleging that the company charged customers unauthorized and marked-up fees. While cases like this are complex and often resolved without admission of wrongdoing, they highlight the importance of transparency in payment processing.

More broadly, payment processing pricing has become a growing topic of concern as businesses push for clearer fee structures and greater accountability.

What Practices Can Do to Protect Themselves

Practices do have options when it comes to protecting themselves from inflated processing costs.

Regularly Review Your Statements

Carefully review your processing statements, especially during months when network rate changes typically occur.

Request Detailed Explanations

If fees increase, request clear explanations showing which fees originate from the card networks and which are processor markups.

Verify Fees with the Card Brands

If you see unfamiliar fees, search for them on the official Visa or Mastercard websites to confirm they actually exist.

Consider Independent Fee Audits

Some organizations hire independent auditing firms to review their processing statements and identify potential overcharges.

The Importance of Transparency in Payment Processing

Payment processing should not feel like a mystery.

When practices understand how their transactions qualify, what interchange actually costs, and how processors generate revenue, they can make better decisions about their payment systems.

Transparent pricing models, modern payment technology, and proper transaction setup can significantly reduce unnecessary costs.

For many practices, the key is working with providers that focus on clear pricing structures, optimized transaction routing, and tools that minimize costly downgrades.

Because when payment processing is transparent, practices can focus on what matters most—serving their patients and growing their organization. For more information on transparent pricing and the savings of dual-pricing, contact PayLow Pro today.